Retirement Planning for Teachers - Sponsored by LGSUHSD's District Teacher's Association (DTA)

|

Understanding CalSTRS

The majority of a teacher's retirement income will come from their California State Teachers Retirement System (CalSTRS) defined benefit pension. To fully understand how STRS works, talk to someone in DTA or go to the STRS web site and sign up for a workshop.

Understanding "The Gap"

Once you understand how STRS works, you will discover that there is something referred to as "The Gap."

The Gap is the difference between your salary (what you earn while working) and the amount of your pension (what you will earn after you retire).

Annuity salespeople use the Gap, especially a person's lack of understanding about the Gap, to frighten them into purchasing high cost, low yield fixed and variable annuities. Talk to your school's teachers association (union) or directly to CalSTRS to learn about low fee options for supplemental investing. This knowledge is essential to make sound investment decisions. Do not respond to emails or calls from people who offer free financial advice. Many will offer a "free" lunch to get you to meet with them. If you invest in their annuities, this might be the most expensive lunch you ever have. Regardless of what they claim, their advice is not free. The products they offer have fees, usually hidden, that are very high. There should never be any pressure to invest. If someone tells you that you must invest NOW...walk away.

Typically your pension will be 35% to 45% lower than your salary. There are several things to understand about planning for the Gap.

1. Your teaching salary includes a 10.25% deduction that you pay to STRS. Your STRS pension does not have this deduction. This decreases the Gap by 10.25%. Annuity sales people will neglect to tell you this.

2. STRS provides an additional source of income beyond your pension. This is your Defined Benefit Supplement (DBS). Your Gap will be further decreased depending on the size of your DBS. Annuity sales people will neglect to tell you this.

3. State, and local taxes will eat into your pension and savings. One important part of retirement planning is considering how taxes will affect your pension and savings. You will pay the same amount of Federal income tax no matter which state you live in. State and local taxes are different in every state, county and city. You will pay state income tax to the state in which you live during retirement. California has one of the highest overall tax rates in the country. Many retirees move out of California to stretch their retirement dollars. If you move out of California, state and local taxes will likely be lower, sometimes significantly. This can help further reduce The Gap. Explore State tax rates.

4. You will need to have additional retirement savings to fully close The Gap and ensure a comfortable retirement. A 403(b) tax-deffered savings plan is the best option for school employees to save for retirement.

The Gap is the difference between your salary (what you earn while working) and the amount of your pension (what you will earn after you retire).

Annuity salespeople use the Gap, especially a person's lack of understanding about the Gap, to frighten them into purchasing high cost, low yield fixed and variable annuities. Talk to your school's teachers association (union) or directly to CalSTRS to learn about low fee options for supplemental investing. This knowledge is essential to make sound investment decisions. Do not respond to emails or calls from people who offer free financial advice. Many will offer a "free" lunch to get you to meet with them. If you invest in their annuities, this might be the most expensive lunch you ever have. Regardless of what they claim, their advice is not free. The products they offer have fees, usually hidden, that are very high. There should never be any pressure to invest. If someone tells you that you must invest NOW...walk away.

Typically your pension will be 35% to 45% lower than your salary. There are several things to understand about planning for the Gap.

1. Your teaching salary includes a 10.25% deduction that you pay to STRS. Your STRS pension does not have this deduction. This decreases the Gap by 10.25%. Annuity sales people will neglect to tell you this.

2. STRS provides an additional source of income beyond your pension. This is your Defined Benefit Supplement (DBS). Your Gap will be further decreased depending on the size of your DBS. Annuity sales people will neglect to tell you this.

3. State, and local taxes will eat into your pension and savings. One important part of retirement planning is considering how taxes will affect your pension and savings. You will pay the same amount of Federal income tax no matter which state you live in. State and local taxes are different in every state, county and city. You will pay state income tax to the state in which you live during retirement. California has one of the highest overall tax rates in the country. Many retirees move out of California to stretch their retirement dollars. If you move out of California, state and local taxes will likely be lower, sometimes significantly. This can help further reduce The Gap. Explore State tax rates.

4. You will need to have additional retirement savings to fully close The Gap and ensure a comfortable retirement. A 403(b) tax-deffered savings plan is the best option for school employees to save for retirement.

Understanding 403(b) plans

A 403(b) plan helps close the gap . Teachers can choose between a tax sheltered annuity (TSA) purchased through an insurance company or a tax sheltered custodial account invested directly in mutual funds. Annuities have high costs and confusing fee structures. They are very profitable for the insurance company and the salesperson who sells the annuity. Often the salesperson will not use the word "annuity." If you are not paying a fee to a financial broker, they are making a commission from fees, usually hidden, that you will be charged.

Four important questions to ask anyone who is selling you something without charging you are: Is this an annuity? What are the total fees? What are the surrender charges? and How many years are surrender charges in effect?

Custodial plan participants will pay significantly less in fees by investing directly in mutual funds.

Four important questions to ask anyone who is selling you something without charging you are: Is this an annuity? What are the total fees? What are the surrender charges? and How many years are surrender charges in effect?

Custodial plan participants will pay significantly less in fees by investing directly in mutual funds.

These articles in the New York Times examine 403(b) annuity plans.

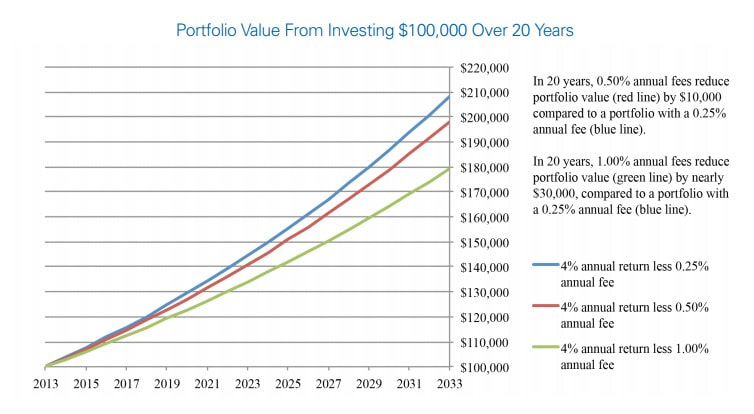

Understanding Fees

High fee 403(b) plans, such as annuities, seriously diminish the amount of an investment's return.

Low fee 403(b) custodial plans increase the power of compounding interest, generating substantially higher returns.

Low fee 403(b) custodial plans increase the power of compounding interest, generating substantially higher returns.

Choosing a 403(b) custodial plan

There are several options for choosing a 403(b) custodial plan. Below are three of the top choices.

CalSTRS

CalSTRS Pension 2 - CalSTRS Pension2 is CalSTRS’ 403(b) plan. Pension2 is a custodial plan that offers an opportunity to invest in low cost, flexible 403(b), Roth 403(b) and 457(b) plans.*

403(b) Compare # 1097

Vanguard

Vanguard Target Date Retirement Index Funds - Use this link to learn about Vanguard's Target Date Retirement funds.*

Vanguard 403(b) Account Application - Use this link to open a Vanguard account. Before you open an account, you must select a fund for your investment.*

403(b) Compare # 1102

California Teachers' Association

CTA Retirement Savings Plan - CTA offers several low cost options for investing.*

403(b) Compare # 1926

Index Funds v. Target Date Funds - Not sure if individual index funds or a target-date fund is right for you? This article can help you decide.

Best Index Funds for Long Term Investing -If you have decided to select individual Index funds, this article is a great place to start researching which funds to select.

Once you have made a decision, you will need to fill out a Salary Reduction Agreement and send it to Amandeep at the district office.

IMPORTANT!!! - This form has a drop down menu that you will use to select where you want your money sent. The menu does not work in the browser. You must download the .pdf and open it in Acrobat Reader for the drop down menu to work.

*The creators of this website are not compensated by Vanguard, CalSTRS or CTA in any way.

CalSTRS Pension 2 - CalSTRS Pension2 is CalSTRS’ 403(b) plan. Pension2 is a custodial plan that offers an opportunity to invest in low cost, flexible 403(b), Roth 403(b) and 457(b) plans.*

403(b) Compare # 1097

Vanguard

Vanguard Target Date Retirement Index Funds - Use this link to learn about Vanguard's Target Date Retirement funds.*

Vanguard 403(b) Account Application - Use this link to open a Vanguard account. Before you open an account, you must select a fund for your investment.*

403(b) Compare # 1102

California Teachers' Association

CTA Retirement Savings Plan - CTA offers several low cost options for investing.*

403(b) Compare # 1926

Index Funds v. Target Date Funds - Not sure if individual index funds or a target-date fund is right for you? This article can help you decide.

Best Index Funds for Long Term Investing -If you have decided to select individual Index funds, this article is a great place to start researching which funds to select.

Once you have made a decision, you will need to fill out a Salary Reduction Agreement and send it to Amandeep at the district office.

IMPORTANT!!! - This form has a drop down menu that you will use to select where you want your money sent. The menu does not work in the browser. You must download the .pdf and open it in Acrobat Reader for the drop down menu to work.

*The creators of this website are not compensated by Vanguard, CalSTRS or CTA in any way.

Some websites to help navigate the fog of retirement planning.

Variable Annuities: What You Should Know - Published by the U.S. Securities and Exchange Commission

The Teacher's Advocate - A Blog by Scott Dauenhauer, a financial planner who works with public school teachers and as a consultant to school plans.

403(b)wise - Created by Dan Otter, author of Teach and Retire Rich, and John Moore, two educators fed up with the lack of objective 403(b) information.

Financial Industry Regulatory Authority - (FINRA) is dedicated to investor protection and market integrity through effective and efficient regulation of the securities industry. You can see if your broker is abiding by fiduciary standards (such as putting your interest first) and to see if there is any legal action pending against them.

The Teacher's Advocate - A Blog by Scott Dauenhauer, a financial planner who works with public school teachers and as a consultant to school plans.

403(b)wise - Created by Dan Otter, author of Teach and Retire Rich, and John Moore, two educators fed up with the lack of objective 403(b) information.

Financial Industry Regulatory Authority - (FINRA) is dedicated to investor protection and market integrity through effective and efficient regulation of the securities industry. You can see if your broker is abiding by fiduciary standards (such as putting your interest first) and to see if there is any legal action pending against them.

For more information and investment advice, these books are available in the library.

|

Teach and Retire Rich by Dan Otter

Teacher Dan Otter lays out exactly how school employees can reap the intrinsic and extrinsic rewards of the profession. Teachers have two 401 (k)-style retirement plans at their disposal. Utilizing concepts illustrated in this book, it is entirely possible for a teacher to retire with hundreds of thousands, and even millions of dollars in savings. The nation is rapidly moving toward an "ownership society" in which the individual must manage most aspects of his or her retirement savings. This book ensures that NO Teacher will be financially left behind. |

|

Millionaire Teacher by Andrew Hallam

This book shows you how to achieve financial independence through smart investing -- without being a financial wizard. Author Andrew Hallam was a high school English teacher. He became a debt-free millionaire by following a few simple rules. In this book, he teaches you the financial fundamentals you need to follow in his tracks. You can spend just an hour per year on your investments, never think about the stock market's direction — and still beat most professional investors. It's not about get-rich-quick schemes or trendy investment products peddled by an ever-widening, self-serving financial industry. |

|

|

Winning With Your 403(b) by Pam Horowitz

Learning how to properly choose and maintain a 403(b) plan can be confusing and downright frightening without the proper information. Winning with Your 403(b) will educate you on this unique and powerful tax-sheltered retirement plan for employees of nonprofit organizations. * Learn why selecting the right 403(b) vehicle is crucial to the success of your investment returns * Pick the 403(b) plan that fits your specific needs by using a 10-point checklist * Select funds to meet the objectives of your 403(b) plan * Develop sound investment strategies that will keep your 403(b) healthy * Steer your 403(b) through job changes, retirement, and beyond Pam Horowitz is a writer, teacher, reading specialist, and expert in 403(b) investing. |